Starting a business will no doubt be among the highlights of your life. Unfortunately, a study conducted by the University of Tennessee found that 44% of companies fail within their first three years of operation. This statistic might dampen your spirits if you are thinking of starting a business or have just started one. Even so, you can learn from the failures of other business owners.

According to Dun & Bradstreet, a credit information bureau, only 10% of businesses close because of bankruptcy. 90% of companies close either because they are set up for the wrong reasons, lack financial power, lack market structure awareness, or do not have a clear focus. All these reasons are attributed to poor planning.

To avoid becoming a statistic among failed startups, start your journey as a business owner by drafting a strategic plan. A strategic plan is in a few ways a form of a business plan.

Though, there are differences between a strategic and a business plan.

A strategic plan is for existing organizations looking to grow their companies, and it entails the direction you need your business to take for the next 3-5 years. It is for managing and implementing the plan for your company. On the other hand, a business plan is for startups and describes what you plan to do in not more than a year. It directs operations or convinces people to invest in your small business.

Strategic plans provide a focus and direction on where you want your organization to go. They are also crucial in planning resources to ensure their efficient use and boost your returns.

You might have a plan in your head on what your business’ future looks like. Even so, you should follow the right steps to ensure it works in your favor and resonates with your objectives.

Key Steps For Strategic Planning for Your Organization

Here are the key steps for strategic planning:

Assess Your Customer Base, Industry, and Competitor Trends

When thinking of a strategic plan, the first step is assessing your customers, industry, and competitors. Also, you cannot ignore the impact of things like pandemic lockdowns, technology, and politics, among other factors, as evidenced in the 2023 Business Outlook Survey Report by LBMC.

Consider how big a factor is, its impact on your business, what your market thinks about it, and how your competitors are responding to it. Think of factors as the ‘’external’’ valuation elements of things that will affect your company.

Conduct A SWOT Analysis

Before you write and communicate your strategic plan, consider your business’s strengths, weaknesses, opportunities, and threats (SWOT). The strengths of your business lie in your financial resources, employees, sales channels, market position, and growth strategies.

{kind=link}

The weaknesses are factors such as missing deliveries, missing products, missing sales channels, client complaints, and dwindling financial resources.

Opportunities comprise the chances of gaining new markets or clients, raising funds for a venture, forming alliances, or launching new products. Threats include losing some of your key staff members, lack of financial resources, falling prices, and unfavorable markets.

Consider the SWOT analysis as an internal and external evaluation of your company. Strength and weakness are internal factors, while opportunity and threats are external factors.

Define Your Vision and Mission

With your external and internal evaluations of the company completed, your next step is to craft a good vision statement coupled with your mission statement. Your mission statement describes why you exist, while the vision speaks about what you are currently offering and what your hopes for the future are.

To create a quarterly vision board for your company, get a cardboard, then split it into four quarters for each quarter of the year with motivating pictures of what you want to achieve.

Write Down Your Corporate Goals

After highlighting what you want to achieve and analyzing your SWOTs, it is important to define your corporate goals. The goals you define in your strategic plan are the specific outcomes for which you are aiming. The goal can be something like improving your product offering, operational efficiency, profits, or sales strategy.

When you organize the action items in your strategic plan into objectives, they remain clear, long after their completion. Above all, ensure all the goals you pick are measurable and time-bound to avoid endless procrastination.

Break Up Goals into Specific Department Action Plans

With your corporate goals in place, ensure that you have specific action plans that you will implement to reach your corporate goal. The drafting of your action plans is best handled by each department to ensure everyone knows the role he/she should play towards attaining a goal and ultimately, your vision.

For instance, if your goal is to improve business morale to help attain maximum profits, one action plan of your HR department might be launching employee benefits.

To avoid departments getting carried away, each department should ideally have specific action items that it can achieve within a specified timeframe. There should also be specific persons to execute the action plan.

Determine Your Financing, Budgeting, and Staffing Needs for Your Business

Even the best strategic plan will not achieve much without the right resources for its execution. Come up with a centralized budget for the action plans of your departments and put in place the required staff for their execution. If your financial resources do not fully meet your expected budget, you can consider lowering the targets in your plan or raising the capital needed to fully actualize your plan.

Communicate the Business Plan

Communicating your strategic plan to the key stakeholders at the appropriate time is crucial for its success. Determine the key players in the plan and know how much information you will give them. In addition, don’t underestimate employee feedback. For example, some of your employees might not need detailed appendices, but you should emphasize the sections in your strategic plans in which they will play key roles.

Give a copy of the strategic plan to your board of directors and senior management. Consider hiring a business coach who can facilitate internal discussions for your plan. After all, you cannot achieve much without 100% cooperation from senior managers. Once the stakeholders know what the plan entails, invite constructive feedback and ideas on it. You can also use the plan to inform your marketing tools and approach to strategies.

With the steps above, you can expect to have the best strategic plan to guide your company. Remember that strategic planning is a process rather than a one-off event. As such, evaluate your progress and the attainment of your goals periodically to ensure the strategic plan is contributing to your vision.

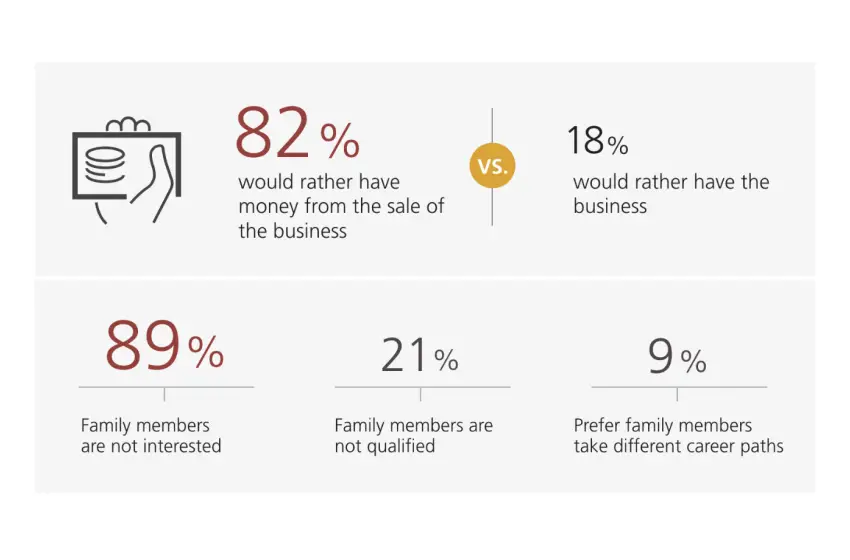

Regardless of the stage of your business, you should have an exit strategy. Think of the company as an asset in which you invest cash. It has a revenue stream supporting your salary and should increase in value to enable you to harvest some extra wealth.

Frictionless: The Right Solution for Your Strategic Planning Process

An exit strategy is a means of transitioning your company to another stage where your role changes. Carefully evaluate your strategic plan and vision, then determine the favorable exit strategy for you. All these steps for running your business might seem challenging without the right technology to help you. Consider a platform like Frictionless that will simplify your strategic growth planning while driving its real-time execution.